Introduction

Financial planning is often described as the art and science of managing money to achieve life goals. While this definition is accurate, it is incomplete without one critical element: insurance. From an executive standpoint, financial planning and insurance are inseparable. One represents growth and direction; the other represents stability and protection. Together, they form the foundation of long-term financial resilience.

As a CEO with extensive experience in financial services and strategic advisory, I have observed a consistent pattern across individuals, families, and organizations. Those who integrate insurance thoughtfully into their financial plans are better prepared for uncertainty, recover more quickly from setbacks, and sustain wealth across generations. Those who neglect protection, regardless of income or investment sophistication, remain vulnerable to risks that can erase years of progress.

This article explores the strategic relationship between financial planning and insurance, emphasizing why insurance should be viewed not as a cost, but as a core financial asset within a comprehensive planning framework.

Financial Planning as a Strategic Process

Financial planning is not a single event but an ongoing process. It involves assessing current financial conditions, defining objectives, identifying risks, implementing strategies, and regularly reviewing outcomes. At its core, financial planning seeks to balance three fundamental priorities: growth, liquidity, and protection.

Many individuals focus heavily on growth through investments while underestimating the importance of protection. From a leadership perspective, this imbalance represents a structural weakness. Growth without protection exposes financial plans to volatility, disruption, and irreversible loss.

Insurance provides the protective layer that allows financial strategies to function effectively over time.

Understanding Risk in Financial Planning

Risk is inherent in every financial decision. Market fluctuations, inflation, longevity, health issues, and unexpected life events all introduce uncertainty. Effective financial planning does not attempt to eliminate risk entirely; instead, it seeks to manage and transfer risks where appropriate.

Insurance is the primary mechanism for transferring financial risk. By paying a predictable premium, individuals can protect themselves against unpredictable and potentially catastrophic losses. This risk transfer is fundamental to financial stability.

From a CEO’s perspective, unmanaged risk is not merely a personal issue—it is a systemic vulnerability.

The Role of Insurance in Financial Stability

Insurance plays a stabilizing role within financial plans by addressing risks that cannot be efficiently managed through savings or investments alone. These risks include premature death, serious illness, disability, property loss, and liability exposure.

By mitigating these risks, insurance helps:

- Preserve accumulated wealth

- Protect income and earning capacity

- Maintain lifestyle continuity

- Support long-term financial objectives

Without insurance, individuals are often forced to liquidate assets, incur debt, or abandon financial goals when adverse events occur.

Life Insurance as a Cornerstone of Financial Planning

Life insurance is one of the most critical components of a comprehensive financial plan. Its primary purpose is income replacement, but its strategic value extends much further.

Life insurance supports financial planning by:

- Providing financial security for dependents

- Covering debts and ongoing obligations

- Funding education and future expenses

- Supporting estate and legacy planning

- Creating liquidity at critical moments

From an executive viewpoint, life insurance is not optional for individuals with financial dependents—it is essential.

Types of Life Insurance and Planning Applications

Different life insurance products serve different planning needs.

Term Life Insurance

Term life insurance offers coverage for a specific period and is typically used to protect temporary financial responsibilities. Its affordability makes it suitable for early and mid-stage financial planning.

Permanent Life Insurance

Permanent life insurance provides lifelong coverage and often includes a cash value component. These policies can support long-term planning goals such as wealth preservation, tax efficiency, and estate planning.

Choosing the right type of life insurance requires alignment with financial objectives, time horizons, and risk tolerance.

Health Insurance and Financial Protection

Health insurance is a fundamental element of financial planning due to the significant financial impact of medical expenses. Healthcare costs can escalate rapidly and unpredictably, posing a major threat to financial security.

Health insurance protects financial plans by:

- Reducing out-of-pocket medical expenses

- Preserving savings and investments

- Ensuring access to quality healthcare

- Minimizing financial stress during illness

From a leadership perspective, health insurance is a prerequisite for sustainable financial planning.

Disability and Income Protection Insurance

Income is the engine of financial planning. Without income, savings and investment strategies quickly unravel. Disability and income protection insurance address this critical risk.

These policies provide financial support when illness or injury prevents individuals from working. They ensure continuity of cash flow and protect long-term financial objectives.

Executives and professionals, whose income potential represents a significant financial asset, should prioritize income protection within their plans.

Property and Liability Insurance in Wealth Protection

Financial planning also encompasses the protection of physical assets and legal exposure. Property and liability insurance safeguard homes, vehicles, businesses, and personal wealth against loss or legal claims.

Adequate coverage ensures that a single incident does not result in disproportionate financial damage. From an executive perspective, asset protection is a non-negotiable element of responsible financial management.

Insurance and Cash Flow Management

Insurance premiums represent ongoing financial commitments and must be managed carefully within a financial plan. Over-insurance can strain cash flow, while under-insurance exposes individuals to risk.

Effective planning involves:

- Prioritizing essential coverage

- Aligning premiums with income stability

- Reviewing policies as circumstances change

Balanced cash flow management ensures that insurance enhances financial resilience rather than undermining it.

Insurance as a Tool for Wealth Preservation

Insurance is often misunderstood as a mechanism for loss recovery rather than wealth preservation. In reality, insurance plays a crucial role in protecting accumulated wealth.

By providing liquidity and risk transfer, insurance prevents forced asset sales, preserves investment strategies, and supports intergenerational wealth transfer.

From a CEO’s standpoint, wealth preservation is as important as wealth creation.

Tax Efficiency and Insurance Planning

In many jurisdictions, insurance offers tax advantages such as deductible premiums, tax-deferred growth, or tax-free benefits. While these features can enhance financial efficiency, they must be approached responsibly.

Tax considerations should support—not dictate—insurance decisions. Regulatory compliance and transparency are essential to maintaining the integrity of financial plans.

Behavioral Challenges in Insurance Decisions

Human behavior plays a significant role in financial planning. Individuals often underestimate risk, delay decisions, or focus on short-term costs rather than long-term benefits.

As a CEO, I emphasize education and structured decision-making. Understanding the role of insurance reduces resistance and encourages proactive planning.

Integrating Insurance into a Comprehensive Financial Plan

Insurance is most effective when integrated into an overall financial strategy rather than treated as a standalone purchase.

Integration involves:

- Coordinating insurance with savings and investments

- Aligning coverage with life goals

- Reviewing protection as circumstances evolve

- Ensuring beneficiaries and ownership structures are current

A holistic approach maximizes the value of both financial planning and insurance.

Financial Planning and Insurance Across Life Stages

Insurance needs change throughout life.

- Early Career: Focus on health and income protection

- Family Stage: Increase life insurance and asset protection

- Mid-Career: Integrate insurance with investment and tax planning

- Pre-Retirement: Review coverage and healthcare needs

- Retirement: Emphasize health, long-term care, and legacy planning

Adaptive planning ensures continued relevance and effectiveness.

Common Mistakes in Financial Planning and Insurance

Some of the most frequent errors include:

- Viewing insurance as an expense rather than protection

- Failing to review policies regularly

- Underestimating coverage needs

- Separating insurance from financial planning

Avoiding these mistakes significantly improves financial outcomes.

The CEO’s Framework for Financial Planning and Insurance

Based on executive experience, a disciplined framework includes:

- Clarifying financial goals

- Identifying financial and personal risks

- Prioritizing essential insurance coverage

- Integrating insurance with long-term strategies

- Reviewing and adjusting plans regularly

This framework supports resilience, flexibility, and sustainability.

Ethical Responsibility and Financial Leadership

Financial planning carries ethical responsibility. Adequate insurance coverage protects not only individuals but also families, businesses, and communities from cascading financial consequences.

Responsible planning reflects foresight, accountability, and leadership.

Long-Term Impact of Integrated Planning

The success of financial planning and insurance is often invisible, measured by stability rather than dramatic outcomes. When protection functions effectively, financial plans remain intact despite adversity.

From a leadership perspective, this quiet resilience represents the highest standard of financial success.

Word Count:

486

Summary:

There are many vital parts of our financial plan: estate planning, mortgages, credit cards, and UK Secured Loans

Keywords:

loans, uk finance

Article Body:

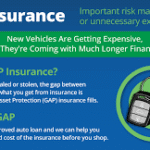

There are many vital parts of our financial plan: estate planning, mortgages, credit cards, and UK Secured Loans. One area you need to include is insurance. Insurance answers the question, “what if something bad happens?� No one likes to think about and too many people avoid the topic of insurance because they fail to see the benefit.

But there is a benefit! With insurance, you will have peace of mind that their loved ones will be taken care of if they die. So why are you reading about insurance on a site that has to do with loans? Simple. You may want to consider insurance to cover your loans so that if you were to pass away, your loved ones will not be saddled with unexpected debt.

And, if you have a secured loan that your loved ones cannot cover, you do not want your assets seized to cover the loan. That will add tragedy to tragedy for your loved ones!

So how do you know what kind of insurance to get to cover your loans? Or any expenses at all, for that matter? The easiest thing to do is to determine the length of time that a particular expense will be present in your life and get insurance that matches the term of the expense.

For example, any death or estate tax will always be present in your life because no matter when you pass away, those expenses will be incurred. Also, if you want to bequeath a gift to a charitable organization, you will likely always want to have that as an available gift to make.

However, for many other expenses, including your loans, a temporary solution is better. For example the mortgage on your house or the loan on your car are both excellent loans to create insurance for. This way, if you were to pass away while these expenses are still present, they will be automatically paid off at your death. And because you are matching the term of the loan to the term of the insurance, you are only buying insurance for as long as you have the loan.

For example, say you have a secured home improvement loan to last for three years while you build an addition onto your home. At the same time you take out a three year term insurance policy for the same amount as the loan.

If you were to pass away in the second year, the insurance would pay your loved ones the full amount of the loan, of which they can use two thirds of it to pay the remaining portion that is still outstanding on your loan.

People do this for many kinds of loans, including their mortgage, their automobile loans, and any other kind of loan they have.

Tinggalkan Balasan